Plantation: Start of a sector 'SELL-OFF' or CPO prices to recover? (Oct 2012)

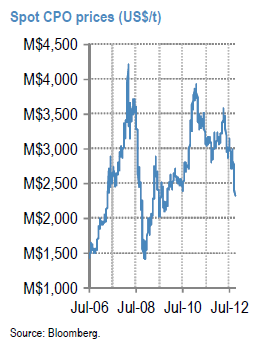

While CPO prices have declined 20% over the past one-month to M$2,300/t, share prices of our upstream plantation universe have not reacted materially moving by -8% to +3% (-3% to +3% for our top picks) Key question hence is whether this raises the risk of a further sell-off in plantation stocks or will CPO prices recover?

Key reasons for the CPO price fall:

1) High inventory levels amid the current high output season.

2) Some easing in demand (though not materially) mainly from slower bio-diesel production.

3) Softening crude oil prices.

4) Better soybean supply prospects with improved weather.

Will CPO prices weaken further?

CPO’s price competitiveness to soy-oil and crude oil is now at its best since the previous economic crisis in late-2008. CPO's price discount is currently at US$340/t to soy-oil (spot) versus its historical mean discount of US$160/t. CPO at current spot levels of M$2,300/t is also already discounting crude oil prices at US$72/bbl based on the bio-diesel breakeven support (spot crude oil price: US$112/bbl).

Hence, we see limited downside risk at these levels and expect CPO prices to recover by 1Q13 as inventories are drawn down during the low output season by end-2012/early-2013 and with substitution demand likely to kick in given the extreme tightness in soybean supply. This is until palm oil and soybean supply recovers from 2Q13 with prices to ease again from then.

|

| The ratio of CPO price (in US$/t) to crude oil price (US$/bbl) has fallen to 7.3x, the lowest level since the previous economic crisis in late-2008 (historical mean ratio of 9.2x). This reflects palm oil's increased competitiveness versus crude oil in the bio-diesel segment. |

Stock recommendations...

We maintain UWs on AALI, IOI, LSIP and GENP and would look to sell these stocks now. Quality stocks like KLK (Neutral) may also be vulnerable short term due to rich valuations. Our key OWs - BWPT, SIME, FR and SIMP are implying 2013E CPO prices of M$2,600-2,700/t at current levels (higher than spot) and could succumb to near term selling pressure – we would look to accumulate on weakness given the support of young plantations and strong volume growth longer term, while SIME remains a defensive large cap play with valuation support.

Source: J.P.Morgan research report

Comments

Post a Comment